Ultimate Guide to ADHD Financial Tools

Practical tools, automation, and simple budgets to cut impulsive spending and simplify money management for adults with ADHD.

Managing finances with ADHD can feel overwhelming, but the right tools and strategies make a big difference. ADHD impacts executive function, leading to challenges like missed payments, impulsive spending, and difficulty maintaining long-term financial goals. The key is to simplify processes, automate tasks, and use tools designed to reduce mental load.

Key Takeaways:

- Challenges: Executive function issues, time blindness, impulsive spending, and difficulty with long-term goals.

- Best Tools:

- Monarch Money: Consolidates accounts for a clear financial overview. ($99.99/year)

- YNAB (You Need A Budget): Zero-based budgeting to control spending. ($109/year)

- PocketGuard: Shows how much you can safely spend today. ($74.99/year for Plus)

- Strategies:

- Use a simple 3-category budget: Bills, Savings, Spending.

- Automate bills, savings, and debt payments to reduce decision fatigue.

- Add visual reminders like savings thermometers or calendar alerts to stay on track.

Quick Tip: Start small - automate one bill or set a reminder for subscriptions. These minor changes can significantly reduce financial stress.

ADHD & Money: Why YNAB Works

sbb-itb-f879324

Financial Challenges for ADHD Professionals

The financial struggles often faced by ADHD professionals aren't just about different ways of thinking - they're tied to how the ADHD brain processes information and makes decisions. Recognizing these challenges is the first step toward finding strategies and tools tailored to your needs.

Executive Function Problems and Money Management

Managing money requires planning, organizing, and remembering - skills governed by executive function. ADHD can disrupt these abilities, making everyday financial tasks feel overwhelming. You might forget to pay bills, even when you have the money, lose track of balances across accounts, or feel stuck when handling multi-step tasks like filing taxes or comparing insurance options.

Working memory issues add another layer of difficulty. For example, you might write a check but forget to record it or start an online payment and get distracted before finishing. Research shows adults with ADHD often score lower in financial comprehension - the ability to grasp the details of financial transactions. As Understood.org explains:

"ADHD doesn't make it hard to understand math or work with money. But it can make it difficult to manage money".

Time blindness, a common ADHD trait, further complicates financial management. According to the "30% rule", individuals with ADHD may have executive function skills about 30% behind their neurotypical peers. This gap can lead to missed deadlines, late fees, and what’s often called the "ADHD tax" - a cycle of costs from forgotten subscriptions, late payments, and interest charges.

On top of these challenges, impulsive emotional responses can make managing money even harder.

Emotional Spending and Impulse Control

Impulse control issues can wreak havoc on a budget. Adults with ADHD are about four times more likely to make frequent impulse purchases compared to those without ADHD, and they tend to carry an average of over $3,000 more in credit card debt. Additionally, up to 21% of adults with ADHD may develop compulsive buying behaviors.

This pattern is tied to altered dopamine pathways in the brain, which drive a need for instant gratification. Shopping can provide a quick dopamine boost, even if the purchase later leads to financial stress. Decision fatigue makes this worse - after a long day of trying to stay focused, your ability to resist impulses weakens. That’s why late-night online shopping often happens not out of need, but because your brain is simply too tired to say no. As psychotherapist Roozbeh Khoshniyat explains:

"impulsive spending is often emotional regulation in disguise".

These impulsive habits make it even harder to stick to long-term financial plans.

Difficulty Maintaining Financial Goals

Staying focused on long-term financial goals can feel almost impossible when immediate rewards seem more appealing. Temporal discounting - a tendency to prioritize short-term gains over future benefits - often leads to spending now instead of saving for later.

By age 30, adults with ADHD earn 37% less per month than their peers. This income gap contributes to a projected retirement shortfall, with individuals with ADHD potentially having 40% to 64% less net worth - around $431,000 less - than their neurotypical counterparts. Finance Professor Chi Liao highlights this financial disparity:

"those with more severe childhood ADHD symptoms are significantly more likely to experience difficulty paying bills, payment delinquency, lack of emergency savings, and delays in purchasing necessities".

Traditional financial advice often falls short because it lacks the immediate feedback that ADHD brains crave. Without tools designed to provide quick, clear tracking, financial setbacks like debt collection or reliance on high-interest payday loans become more common.

Best Financial Tools and Apps for ADHD

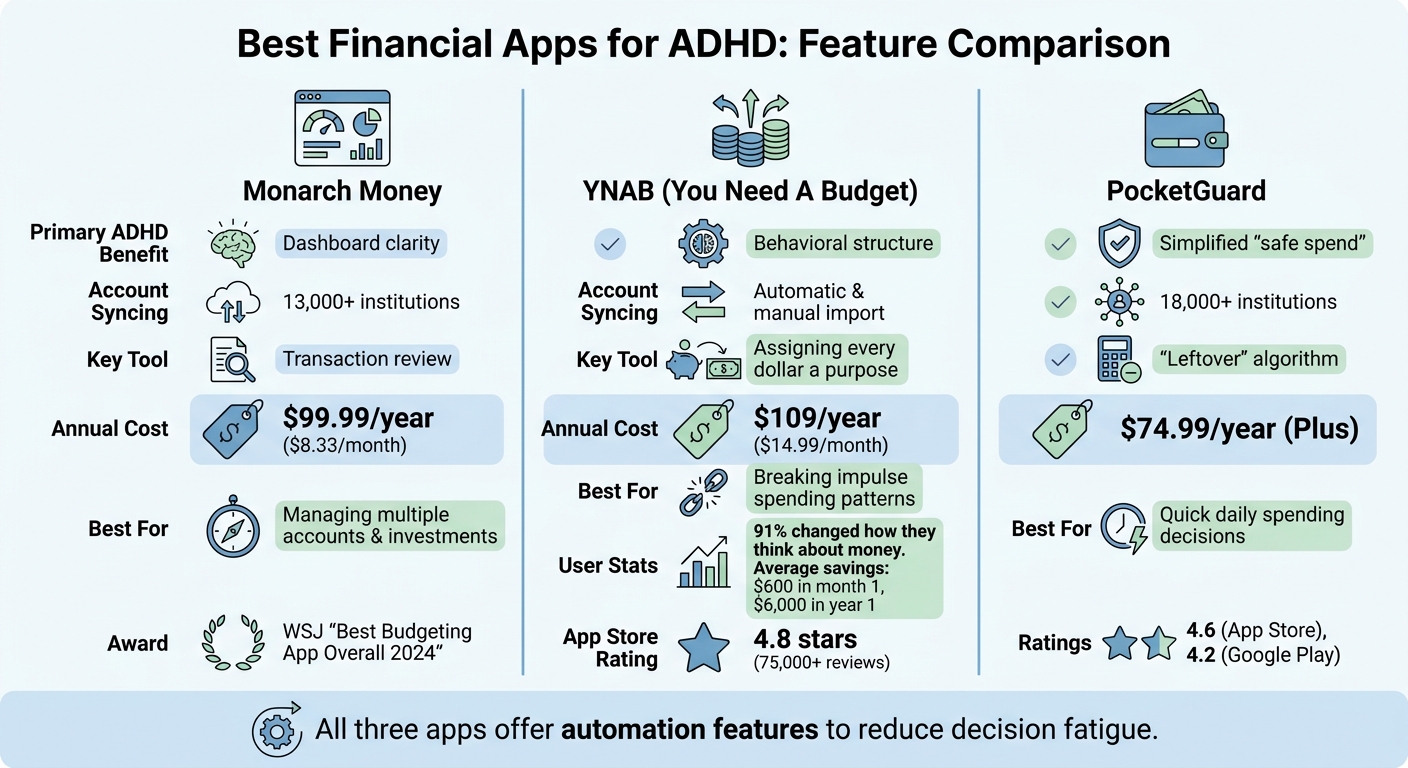

ADHD Financial Apps Comparison: Monarch Money vs YNAB vs PocketGuard

Managing finances can be a daunting task, especially when ADHD adds layers of complexity. The good news? Some apps are designed to lighten the mental load and make money management more straightforward. The right app can take the stress out of tracking finances, giving you a clear picture of your financial situation. For those with ADHD, automation and simplicity are key. Here are three standout tools: Monarch Money, YNAB (You Need A Budget), and PocketGuard.

Monarch Money: All Your Accounts in One Place

Juggling multiple bank accounts, credit cards, and investments can feel overwhelming. Monarch Money tackles this by consolidating all your financial accounts into a single, easy-to-navigate dashboard. With connections to over 13,000 financial institutions, it automatically categorizes transactions and flags recurring subscriptions, helping you stay on top of your spending without the mental drain.

One of its standout features is the ability to mark purchases as reviewed, which helps reduce decision fatigue. Monarch Money’s design has even earned it recognition from The Wall Street Journal as the "Best Budgeting App Overall for 2024", particularly for those managing diverse financial priorities.

The app costs $99.99 annually (around $8.33 per month) or $14.99 monthly, and it even includes free partner access. If you’re looking for a tool to centralize your finances, Monarch Money is worth considering.

YNAB (You Need A Budget): Assign Every Dollar a Purpose

YNAB takes a proactive approach to budgeting with its zero-based system, where every dollar is given a specific job before you spend it. This method is particularly effective for combating impulsive spending and planning challenges often associated with ADHD. Features like "Targets" let you break down large, irregular expenses - think annual insurance payments or unexpected car repairs - into manageable monthly goals.

The impact of YNAB is clear: 91% of its users say it changed how they think about money, and 92% report feeling less financial stress. On average, users save $600 in their first month and $6,000 in their first year. Take Kyle, for example. He started 2020 with just $37 in savings but, by sticking to YNAB’s system, ended the year with $42,000 saved. He even managed to pay $14,000 in cash for a new roof, avoiding debt entirely. As Kyle put it:

"YNAB has removed the stress of money from my life and in doing so has helped make me a better husband. It's like I got to remove a personal flaw I had never been able to fix".

YNAB costs $109 per year or $14.99 monthly, with a 34-day free trial to test it out. The app also makes it easy to stay organized with pinned categories, a flexible setup checklist, and the option to share your budget with up to five people. With a 4.8-star rating on the App Store from over 75,000 reviews, YNAB is a strong choice for those seeking structure in their financial lives.

PocketGuard: Know What You Can Spend Today

For quick, everyday spending decisions, PocketGuard is a game-changer. It simplifies budgeting by showing you one key number: how much you can safely spend right now. This "In My Pocket" (or "Leftover") feature calculates what’s available after factoring in bills, savings goals, and other essentials. This clarity helps ADHD professionals avoid decision fatigue and overspending. Financial writer Ben Luthi describes it well:

"PocketGuard's Leftover feature clearly shows how much you can spend after bills and savings, making it perfect for overspenders".

The app connects securely to over 18,000 financial institutions. While the free version limits you to syncing two accounts, the Plus version offers expanded features for $12.99 per month, $74.99 annually, or a one-time lifetime fee of $149.99. With ratings of 4.6 on the App Store and 4.2 on Google Play, PocketGuard is ideal for those who need a straightforward tool for daily financial decisions.

| Feature | Monarch Money | YNAB | PocketGuard |

|---|---|---|---|

| Primary ADHD Benefit | Dashboard clarity | Behavioral structure | Simplified "safe spend" |

| Account Syncing | 13,000+ institutions | Automatic & manual import | 18,000+ institutions |

| Key Tool | Transaction review | Assigning every dollar a purpose | "Leftover" algorithm |

| Annual Cost | $99.99/year | $109/year | $74.99/year (Plus) |

| Best For | Managing multiple accounts & investments | Breaking impulse spending patterns | Quick daily spending decisions |

ADHD Budgeting Strategies That Work

Building on the challenges and tools discussed earlier, these budgeting strategies are designed to align with how your brain naturally operates. As Harold Robert Meyer, Founder of The A.D.D. Resource Center, puts it:

"Traditional budgeting fails spectacularly for ADHD brains because it demands sustained attention, detailed tracking, and fights against how your brain naturally works."

The methods below aim to reduce mental effort, cut down on decision fatigue, and create systems that practically run themselves.

Simple 3-Category Budget

Forget the headache of detailed spreadsheets. The Three Buckets System simplifies budgeting by dividing your money into just three accounts:

- Bills: Covers fixed expenses like rent and utilities.

- Savings: Reserved for future goals and emergencies.

- Spending: For everyday purchases.

Here’s how it works: Your Bills Account holds only what’s needed for fixed costs (usually 40%-60% of your income) and doesn’t come with a debit card, so accidental spending is off the table.

Savings? That goes into an account at a separate bank. This setup adds a 2–3 day delay for transfers, which can help cool off impulsive spending urges - studies suggest this reduces such spending by 50%.

Finally, your Spending Account is the only one linked to a debit card. Once the balance hits zero, it’s a clear signal to stop spending. This system removes the guesswork and helps avoid accidental debt.

Automate Everything You Can

Automation takes the pressure off your executive function. You’re not relying on memory or willpower to save or pay bills - it all just happens. As Ramit Sethi, author of I Will Teach You To Be Rich, explains:

"Financial automation transforms money management from a constant mental burden into a background process that works whether you remember it or not."

Start by splitting your direct deposits so your paycheck automatically routes to your Bills, Savings, and Spending accounts as soon as it hits. Then, schedule all bill payments and savings transfers for the day after payday. This timing helps avoid late fees and interest charges - what’s often called the "ADHD tax".

Automation can handle up to 90% of the financial tasks ADHD individuals often struggle with. Even automating minimum payments on debts and credit cards ensures on-time payments, protecting your credit score from forgetfulness. And don’t forget to set a yearly reminder to review subscriptions - canceling unused ones can save you from quietly losing money.

Visual Cues and Reminders

While automation takes care of the routine, visual cues provide a constant, tangible connection to your financial progress. These reminders are especially helpful for ADHD minds that thrive on immediate feedback.

Consider creating a physical savings thermometer to track progress toward your goals. Filling it in triggers dopamine, making saving feel more like a rewarding game. Use color-coded categories in budgeting apps - for instance, red for bills and green for savings - to make your financial standing instantly clear. You could also keep a "Wins" album on your phone with screenshots of milestones like growing savings balances to give yourself a quick motivational boost.

Set calendar alerts at least three days before bills are due to combat time blindness. Enable low-balance alerts and push notifications in your banking apps to stay aware of your financial status. Sticky notes in visible spots - on your desk or phone - can serve as reminders for weekly financial check-ins. These small, visual nudges help you stay on track without relying solely on memory or willpower.

Using On/Off Genius for Financial Consistency

On/Off Genius isn't just another budgeting tool; it’s designed as a cognitive support system to help you maintain consistency in managing your finances. While financial apps and automation can handle the technical side of money management, staying consistent is often the real challenge - especially for professionals with ADHD. This platform aims to remove the distractions that derail financial habits, giving you the mental space to focus.

Building Long-Term Financial Habits

The main hurdle in consistent financial management isn’t a lack of knowledge - it’s the mental clutter caused by competing priorities. On/Off Genius steps in by automating non-financial tasks, so you can direct your energy toward regular financial check-ins.

By outsourcing these "life admin" tasks, you safeguard your executive function for critical financial activities. For example, the time and energy you save can be used to establish a simple weekly ritual, like a 10-minute "money minute", where you review your finances. With fewer mental interruptions, it becomes easier to stick to this habit. This approach also tackles time blindness by creating a clear boundary between personal and professional responsibilities.

The platform also helps streamline tasks like reviewing automatic payments and subscription services, reducing the risk of hidden costs. By eliminating distractions, you’re more likely to complete these reviews instead of pushing them off indefinitely.

With these habits in place, you’ll find it easier to stay focused and make sound financial decisions.

Focus and Organization Tools

When it comes to complex financial decisions - like comparing insurance plans - focus is key. On/Off Genius helps by managing personal distractions that can pull you away mid-task. This reduces the mental fatigue that comes from constantly switching between responsibilities.

You can use the platform to schedule dedicated financial planning sessions, confident that personal tasks won’t interfere. It creates a distraction-free environment, so when you’re working on your finances, you’re not worrying about booking appointments or handling unrelated errands. By offloading these non-financial concerns, you preserve your mental energy for decisions that truly impact your financial well-being.

On/Off Genius works alongside other financial apps, offering the structure and focus you need for uninterrupted financial planning.

Conclusion

Handling finances with ADHD isn’t about forcing yourself into rigid budgeting methods - it’s about creating systems that align with how your brain works. For instance, automating tasks can take care of up to 90% of the repetitive actions that might otherwise overwhelm you. On top of that, visual tools can help you better understand and track your financial habits.

Here’s the key: automate what’s possible, use the Three Buckets system to simplify decisions, and introduce some friction to help prevent impulsive spending. As Harold Robert Meyer, Founder of The A.D.D. Resource Center, wisely states:

"The goal isn't perfection - it's protection from your future impulsive self while giving your current self permission to enjoy life".

To start, focus on small but impactful changes. Set up one automation, like recurring savings or autopay for a single bill. Try the 24-hour rule to pause before making impulsive purchases. Then, incorporate a quick 5-minute payday ritual to double-check your automations and celebrate small victories.

By using these systems and tools like On/Off Genius for cognitive support, you can reduce the time spent on financial management to just five minutes per pay period. That leaves you with more energy to focus on the things that truly matter to you.

These strategies are designed to turn financial disarray into easy-to-follow steps. As Brynne Conroy puts it:

"The good news is that you may not be bad with money at all. You've just been using strategies that don't accommodate your neurodivergence".

You’ve got the tools and strategies - now it’s time to put them into action.

FAQs

Which budgeting app is easiest for ADHD?

HyperJar stands out as a helpful tool for managing finances, especially for individuals with ADHD. Its color-coded jars provide a clear and visual way to organize spending. Features like spending limits, automated payments, and the ability to block certain retailers add extra layers of simplicity and control.

Another option is Cake Budget, which uses a traffic light system - green, amber, and red - to guide spending decisions in real time. This straightforward design gives instant feedback, making it easier for ADHD minds to stay on track with budgeting through visual cues and an easy-to-use interface.

How do I start automating bills and savings?

Managing finances can feel overwhelming, but automating key tasks can make it a lot easier. Here’s how you can streamline your bills and savings:

- Set up automatic payments: Most banks and service providers offer options to automate payments. This ensures you never miss a due date and helps avoid late fees.

- Use calendar reminders: Even with automation, staying in the loop is important. Set up alerts a few days before payments are due to keep track of everything.

- Automate your savings: Arrange for a portion of your paycheck to go directly into your savings account or schedule regular transfers. This way, saving becomes effortless.

These small adjustments can take a huge burden off your shoulders, making financial management less stressful - especially for those juggling ADHD or a busy schedule.

How can I stop impulsive spending fast?

To tackle impulsive spending effectively, try adding a pause and introducing friction into your buying habits. For example, keep a straightforward plan or reminder visible when making decisions, and set up small obstacles to slow down impulsive purchases. These tactics are particularly useful during moments when you're feeling tired, stressed, or bored - situations that often lead to ADHD-related spending. By doing this, you can make more thoughtful choices without depending entirely on willpower.